Another High Contract for Stuyvesant Heights

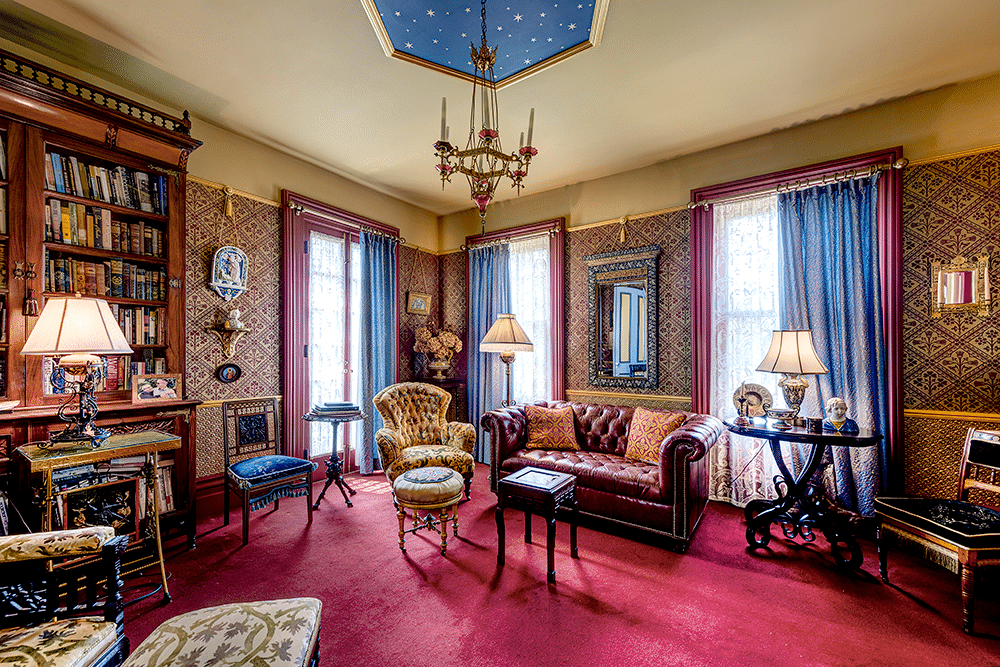

A stunning Magnus Dahlander home with beaucoup original details at 242 Decatur Street is now in contract for $1.75 million all cash, we hear. The sellers were asking $1,800,000. Photos by Evans & Nye

A stunning Magnus Dahlander home with beaucoup original details at 242 Decatur Street is now in contract for $1.75 million all cash, we hear. The sellers were asking $1,800,000.

Photos by Evans & Nye

Thank you!